Energy Market Outlook

This edition explores recent developments in the energy markets and provides an overview of select energy ETFs to consider.

Oil prices have soared in recent trading sessions, yet energy equity investors have been very cautious this week.

Are we heading for another oil bull market, similar to the one that followed Russia’s invasion of Ukraine?

This edition explores recent developments in the energy markets and provides an overview of select energy ETFs to consider.

Energy Market Volatility Ahead

Energy markets have had a very rocky decade. Oil briefly launched into the negatives in 2020, before soaring in 2022 on the back of geopolitical tensions. Oil equities approached a solid bottom in 2020-2021, and have since rallied strongly in the past five years, even though the price of oil has been much lower following the recent spike in the past week.

The State Street Energy Select Sector SPDR ETF has rallied by around 120% in the past five years, but has been flat this week following new geopolitical tensions.

The next couple of weeks should be very telling of where energy equities are heading in the long run. Any sustained geopolitical conflicts could send oil equities into a massive bull market, although returns have so far been very muted in recent trading sessions.

Recent Developments this Week

Geopolitical tensions in the Middle East have resulted in oil prices advancing to break $90/barrel on Friday, March 6th.

Many market participants may be reminded of similar tensions in Russia and Ukraine, and how this resulted in an oil price spike in 2022. Although oil prices have approached this similar high in the past weeks, energy equities have not rallied.

OPEC has responded by planning slight hikes in production in April, although this has not stopped the oil price from rallying this week.

One key concern is that the Strait of Hormuz controls around 20% of oil shipments, and that a potential long-term supply disruption in this route could cause oil prices to soar. Trump’s call for an unconditional surrender from Iran on Friday further elevated the energy markets, as prolonged regional conflicts could result in a long-term increase in the price of oil.

Transportation security is another crucial area to monitor. Trump has stated that the US may provide naval insurance and escorts to help appease the price of oil, but this has not stopped oil’s recent rally this week.

As usual, this likely comes down to duration. It is currently unclear how long tensions in the Middle East will last, which is one of the reasons why the equity performance of energy stocks has been relatively flat this week despite massive gains in the price of oil.

Limited Moves from Equities: Global Implications

Oil equities have had limited gains during the past week, even though the price of oil has soared from under $70/barrel to over $90/barrel this week.

|

ETF |

5 Day Return |

|

State Street Select Energy SPDR ETF |

+0.32% |

|

VanEck Oil Services ETF |

-4.33% |

|

State Street SPDR S&P Oil and Gas

Production ETF |

+4.94% |

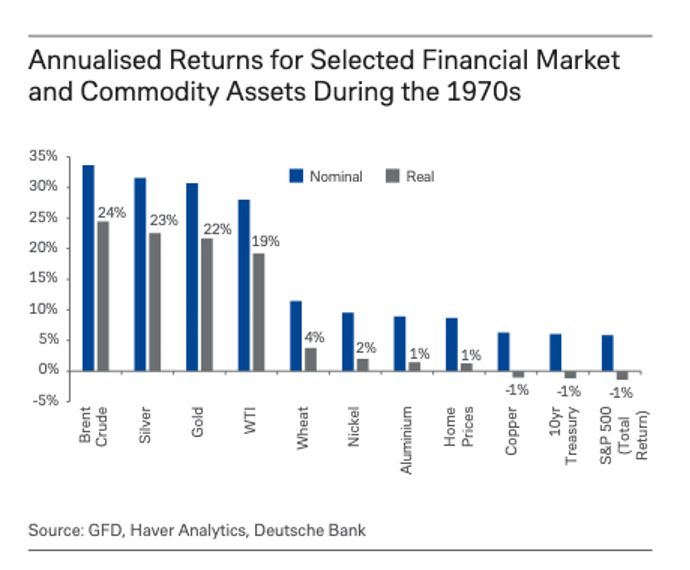

A relevant past benchmark is Russia’s invasion of Ukraine in early 2022, which sent energy markets into a brief but fierce bull market during the following months after this event. However, this did not create a more lasting bull market than we have seen in previous market cycles, such as the 1970s.

If the situation in the Middle East turns into a long and drawn-out conflict, this could have massive implications for the divergence of performance in equities. During the 1970s, commodities performed very well, while the S&P 500 had weak performance and did not begin to recover strongly until the early 1980s.

Regardless of what happens, diversifying into commodities could be a solid portfolio hedge in 2026 and beyond. A commodities bull market could have a negative impact on global economic and equity sentiment.

A prolonged increase in the price of commodities would harm many developed economies, like the United States and Europe, which were beginning to consider additional rate cuts. Similarly, many emerging markets, especially net energy importers, could stand to struggle in this scenario. A lower growth and higher inflationary period could harm global equity sentiment for traditional sectors if there is a prolonged energy bull market.

While energy only comprises less than 4% of the S&P 500, this has been as high as 16% in previous cycles. There could be a stronger shift of focus in the coming years, away from dominant themes like IT and more toward themes like energy and materials.

Examining Energy ETFs

There are plenty of energy ETFs to check out this week and potentially consider, as there is more clarity about the energy market outlook in the coming months.

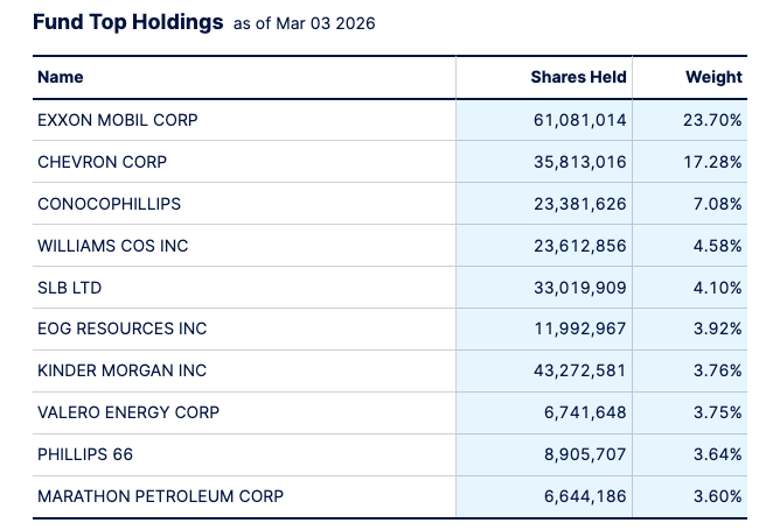

One of the largest ETFs to consider is the State Street Energy Select Sector SPDR ETF, which charges a 0.08% management fee and invests in 22 leading energy companies. This ETF provides concentrated exposure to some of the leading names in the market, including Exxon and Chevron Corporation.

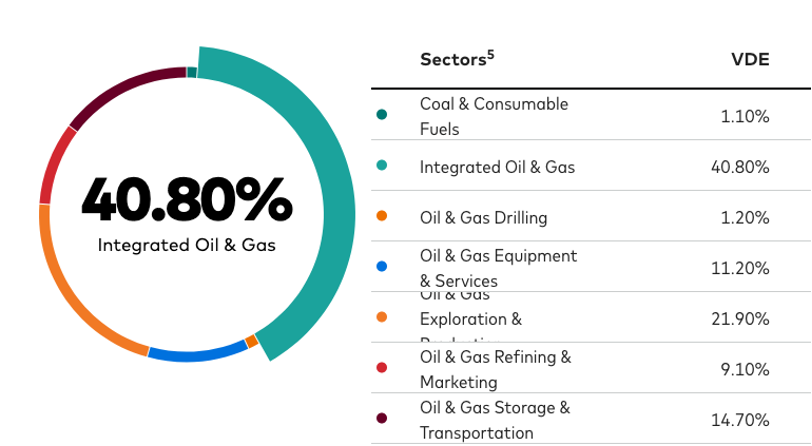

The Vanguard Energy ETF is another low-fee option to consider, which invests in some of the same names as the previous ETF. However, this ETF is much more diversified as it targets over 100 companies in the energy sector.

Midstream companies can also be a more stable bet, and the Global X MLP & Energy Infrastructure is a solid vehicle to consider. This ETF invests in midstream infrastructure companies, including pipelines and storage facilities. This approach is generally considered more conservative, as it can be less sensitive to volatility in energy prices.

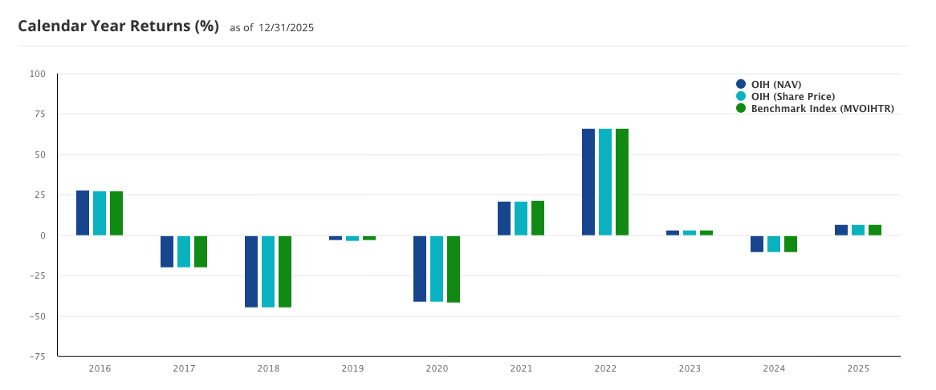

Another unique way to gain exposure to the market is to consider a basket of oil services companies. The VanEck Oil Services ETF tracks the performance of companies operating in areas like oil services, oil drilling, and oil equipment. This ETF has flown under the radar following its strong breakout amid higher oil prices in 2022.

The next couple of weeks could result in a new trend of divergence in performance among various energy sectors. Energy is one of the few S&P 500 sectors that could become more relevant if sentiment shifts to focus more on commodities.